Customer Validation and ROI-Driven Intel Manufacturing Strategy Transformation: Post-Q2 Earnings Analyst Insights on Potential Fabless Shift and Semiconductor Ecosystem Impact 客户验证与回报驱动Intel制造战略转型:Q2财报会议后分析师解读潜在Fabless化及对半导体生态的影响

Key Logic Overview 核心逻辑概述

Multiple analyst reports indicate that Intel clearly articulated a significant shift in its manufacturing strategy during its Q2 earnings call: future capital expenditures will strictly depend on customer validation and capacity reservations. Investments in 14A and subsequent processes will only proceed if acceptable return on investment is achievable for external customer business. This strategy is interpreted by the market as a "challenge" to external customers and the US government, emphasizing that external support is crucial for Intel's diversity in leading-edge foundry and for US strategic technological advantage. It also hints at a potential future shift towards a more Fabless model. Although Intel's Q2 revenue benefited from demand pull-forward driven by tariffs, gross margins remain under pressure, and its strategic transformation is slow, lacking short-term catalysts. This has led analysts to maintain a cautious outlook on its future performance and investment ratings. The move is also expected to have a generally negative impact on the semiconductor equipment market (especially the EUV supply chain), while benefiting foundries like TSMC and Samsung Foundry and their related material suppliers. 多份分析师报告显示,Intel在Q2财报会议上明确了其制造战略的重大调整,即未来的资本支出将严格依赖客户验证和产能预订,并且只有在14A及后续工艺能获得可接受的投资回报时,才会继续投入外部客户业务。这一策略被市场解读为Intel向外部客户和US government发出的“挑战书”,旨在强调外部支持对其在领先晶圆代工领域的多样性和US战略技术优势的重要性,同时也暗示了其未来可能转向更侧重Fabless模式的趋势。尽管Intel的Q2营收表现受益于关税驱动的需求前置,但毛利率持续承压,且其战略转型过程缓慢,缺乏短期催化剂,这导致分析师对其未来业绩和投资评级持谨慎态度,并认为此举将对半导体设备市场(特别是EUV供应链)产生普遍负面影响,同时利好TSMC和Samsung Foundry等代工厂及其相关材料供应商。

Intel Manufacturing Strategy Core Shift & Financial Performance Analysis Intel制造战略的核心转变与财务表现解析

Capex Deployment Tied to Customer Validation & ROI 资本支出部署严格依赖客户验证与回报

Intel announced that its capital expenditure (capex) deployment will be strictly dependent on customer validation and reservations for required capacity. Intel宣布其资本支出(capex)的部署将严格依赖客户验证以及对所需产能的预订。

14A Process Investment Condition 14A工艺投资条件

Intel explicitly stated that investment in its 14A process (expected to enter mass production in 2028-2029) will only proceed if it yields acceptable capital returns, driven by both its own products and meaningful external customers. Morgan Stanley analysts were surprised by this, as Intel had previously suggested its foundry business could break even without external customers. Intel明确表示,只有当其自有产品和有意义的外部客户共同驱动14A工艺获得可接受的资本回报时(预计在2028-2029年量产),公司才会进行投资。Morgan Stanley对此表态表示惊讶,因为Intel曾表示即使没有外部客户,其代工业务也能实现盈亏平衡。

Process Progress & Capacity Outlook 工艺进展与产能展望

-

J.P. Morgan analyst Harlan Sur noted Intel's reaffirmation of commitment to wafer manufacturing. The 18A process continues to advance and is planned for Intel's next 3 generations of products. The first skew for the 18A process is anticipated with the Panther Lake processor by year-end. J.P. Morgan分析师Harlan Sur指出,Intel重申对晶圆制造业务的承诺:18A工艺仍在取得进展,并计划用于Intel未来3代产品。18A工艺的第一个skew预计将于今年年底随Panther Lake处理器一同推出。

18A Capacity Ramp-Up Slowdown 18A产能爬坡缓慢

The 18A process capacity ramp-up will be significantly slower, with peak capacity not expected until the early 2030s. 尽管如此,18A工艺的产能爬坡速度会慢很多,其峰值产能预计要到2030年代早期才能实现。

-

14A process development is on track, with the company learning from mistakes made with 18A foundry operations. The focus for 14A is on gaining external customer validation and addressing broader market needs. 14A工艺的开发正在顺利进行,公司正在从18A代工业务中汲取的错误中学习。14A的重点是获得外部客户的验证,并解决更广泛的市场需求。

-

Intel is curbing the fragmentation of its manufacturing business, halting projects in Germany and Poland, and consolidating operations in Costa Rica to create a more streamlined manufacturing footprint. Intel正在遏制制造业务的碎片化,停止了在Germany和Poland的制造项目,并将业务整合到Costa Rica,以创建更精简的制造足迹。

Analyst Outlook: Risk of Abandoning Leading-Edge Foundry 分析师展望:放弃领先晶圆制造业务的风险

Both J.P. Morgan and Bernstein believe Intel's comments imply that if an acceptable return is not achieved, Intel might abandon its leading-edge wafer manufacturing business, posing a risk to the semi-cap industry. J.P. Morgan和Bernstein均认为,这一评论暗示,如果无法实现可接受的回报,Intel可能会放弃领先的晶圆制造业务,这对semi-cap行业构成一定风险。

Analyst Interpretation & Potential Impact of Intel's New Strategy 分析师对Intel新策略的解读与潜在影响

Intel's Intent: A "Challenge" and a "Cry for Help" Intel的意图:“挑战书”与“求援信号”

J.P. Morgan: A Fair & Reasonable "Challenge" J.P. Morgan:公平合理的“挑战书”

J.P. Morgan analyst Harlan Sur views Intel's pursuit of acceptable ROI as a fair corporate stance. He interprets Intel's explicit statement—that it won't invest in 14A without "meaningful external customers"—as a "challenge" to clients to actively collaborate. It also sends a message to the US government: if external customers aren't secured, Intel won't invest in strategically vital leading-edge semiconductor tech for the US. J.P. Morgan分析师Harlan Sur认为,Intel追求可接受的投资回报是一个非常公平且合理的公司视角。他指出,Intel明确表示除非有“有意义的外部客户”,否则不会进行14A投资。这向外部客户和潜在客户发出了“挑战书”:他们需要在此阶段积极与Intel合作,帮助其改进工艺,使其成为内部和外部客户均可使用的工艺。J.P. Morgan认为,这可能也是在向US government传递信息:如果没有外部客户,Intel将不会投资对US至关重要的领先半导体技术。

Bernstein: Covert Threat or Cry for Help? Bernstein:隐性威胁还是求援信号?

Bernstein analysts suggest that Intel's move could be a thinly veiled "cry for help" to the government, potentially accompanied by an implicit threat regarding future investments. Bernstein分析师提出,一种半合理的观点认为,Intel此举是对政府的求援信号,并带有隐性威胁。

Potential Shift Towards a "Fabless" Model 转向“Fabless”模式的可能性

-

Morgan Stanley analysts believe Intel's "half-hearted" stance on its Foundry business might drive it towards a more Fabless strategy. Morgan Stanley分析师认为,Intel这种对Foundry业务“半心半意”的态度,可能导致其转向更偏向“Fabless”的策略。

-

J.P. Morgan (in a second report) indicates that Intel is moving towards a more Fabless model within the next 3-4 years, which they view as a positive development. J.P. Morgan(第二篇报告)指出,Intel未来3-4年内将转向一个更加Fabless的模式,分析师认为这是一个积极的进展。

-

Bernstein analysts suggest that while Intel remains committed to its current 18A node, abandoning future advanced nodes implies Intel could eventually become a Fabless company. Bernstein分析师指出,尽管Intel仍将致力于当前的18A节点,但放弃未来更先进节点表明Intel最终可能成为一家Fabless公司。

-

Morgan Stanley believes this stance effectively rules out Intel's return to the "IDM 1.0" model 5 years from now. Morgan Stanley认为,这种表态有效地排除了Intel在5年后回归“IDM 1.0”模式的可能性。

Challenges to Intel's Own Operations 对Intel自身运营的挑战

Self-Fulfilling Prophecy for Customer Attraction 客户吸引的自我实现预言

Bernstein analysts argue that by disclosing this information, Intel might make it harder to attract major customers, as clients could doubt its commitment, potentially becoming a self-fulfilling prophecy. Bernstein分析师指出,Intel自身披露这一信息可能反而使其更难吸引主要客户,因为客户可能对其承诺产生疑虑,这可能成为一个自我实现的预言。

Double Disadvantage: Capital Expenditure & Gross Margin Loss 双重劣势:资本支出与毛利率损失

Bernstein believes that maintaining 18A while abandoning 14A brings a double disadvantage: 18A still requires capital expenditure, and outsourcing will lead to potentially significant incremental gross margin losses. Bernstein分析师认为,目前保留18A同时放弃14A,可能同时带来了两方面的劣势:18A仍需要资本支出,而外包将带来可能显著的增量毛利率损失。

Slow Transformation & Market Share Erosion 转型缓慢与市场份额侵蚀

J.P. Morgan highlights that Intel's multi-year transformation is progressing slowly, during which it will continue to consume cash and cede more market share in PC Client and Server businesses to AMD. J.P. Morgan(第二篇报告)指出,Intel的多年转型故事进展缓慢,在此期间,Intel将继续消耗现金,并在PC Client和Server业务领域向AMD让出更多市场份额。

Lessons from Past Capex: $90 Billion Spent, Minimal Revenue Gain 过往资本支出的教训:900亿美元投资,营收增量甚微

Morgan Stanley notes that Intel's new CEO Pat Gelsinger may adopt a more conservative strategy, learning from the previous management team's "5 nodes in 4 years" plan, which led to $90bn in capital expenditures but yielded minimal revenue growth. Morgan Stanley指出,Intel新任CEO Pat Gelsinger可能采取更保守的策略,吸取前任管理团队的教训,即前任“5节点4年”计划导致Intel投入了$90bn的资本支出(约合900亿美元),使公司陷入财务困境,但营收增量甚微。

Intel Strategy Adjustment's Far-reaching Impact on Semiconductor Ecosystem Intel战略调整对半导体生态系统的深远影响

Impact on Wafer Fab Equipment (WFE) Market 对晶圆制造设备(WFE)市场的影响

Bernstein analysts believe that Intel's potential abandonment of advanced nodes is a negative factor for the entire WFE market, especially the EUV supply chain. Bernstein分析师认为,Intel的潜在放弃对整个WFE市场,尤其是EUV供应链,是负面因素。

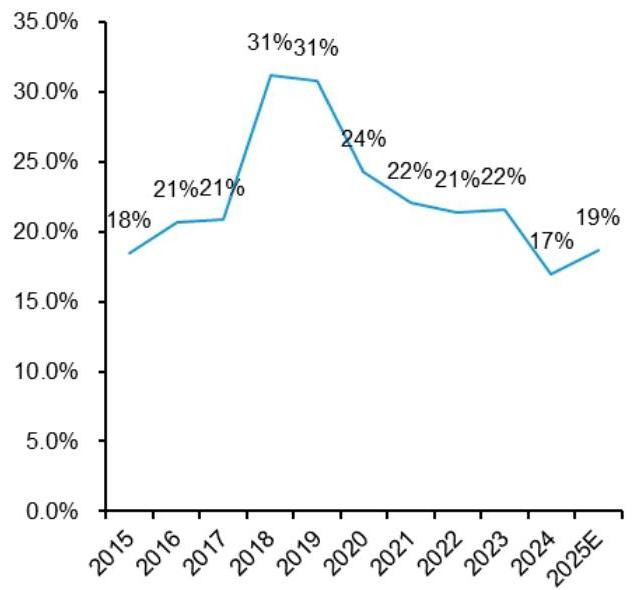

Intel Capex as % of Logic/Foundry Capex Intel资本支出占逻辑/晶圆代工资本支出的百分比

Source: Gartner, Company data, Bernstein estimates and analysis. 来源:Gartner,公司数据,Bernstein估算与分析。

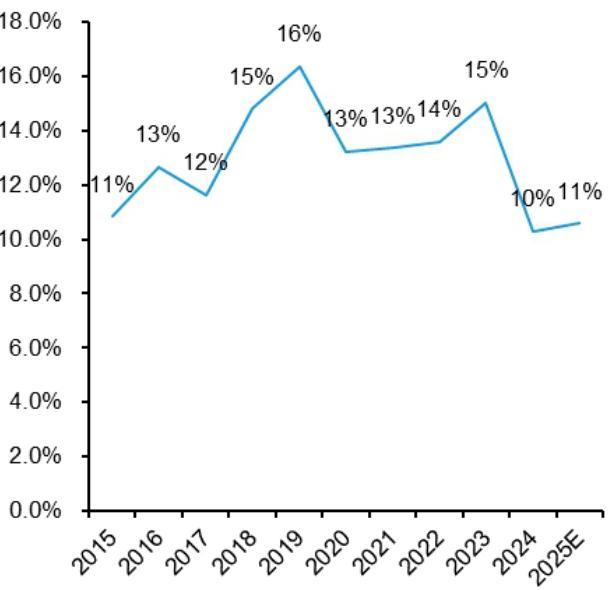

Intel Capex as % of Total Semiconductor Capex Intel资本支出占总半导体资本支出的百分比

Source: Gartner, Company data, Bernstein estimates and analysis. 来源:Gartner,公司数据,Bernstein估算与分析。

Intel is a major semiconductor capital spender, contributing 20-25% of logic/foundry capital expenditure and 10-15% of total semiconductor capital expenditure. Its importance extends significantly to the EUV supply chain. Intel是主要的半导体资本支出方,其资本支出贡献了逻辑/晶圆代工资本支出的20-25%,以及总半导体资本支出的10-15%。Intel对EUV供应链尤为重要。

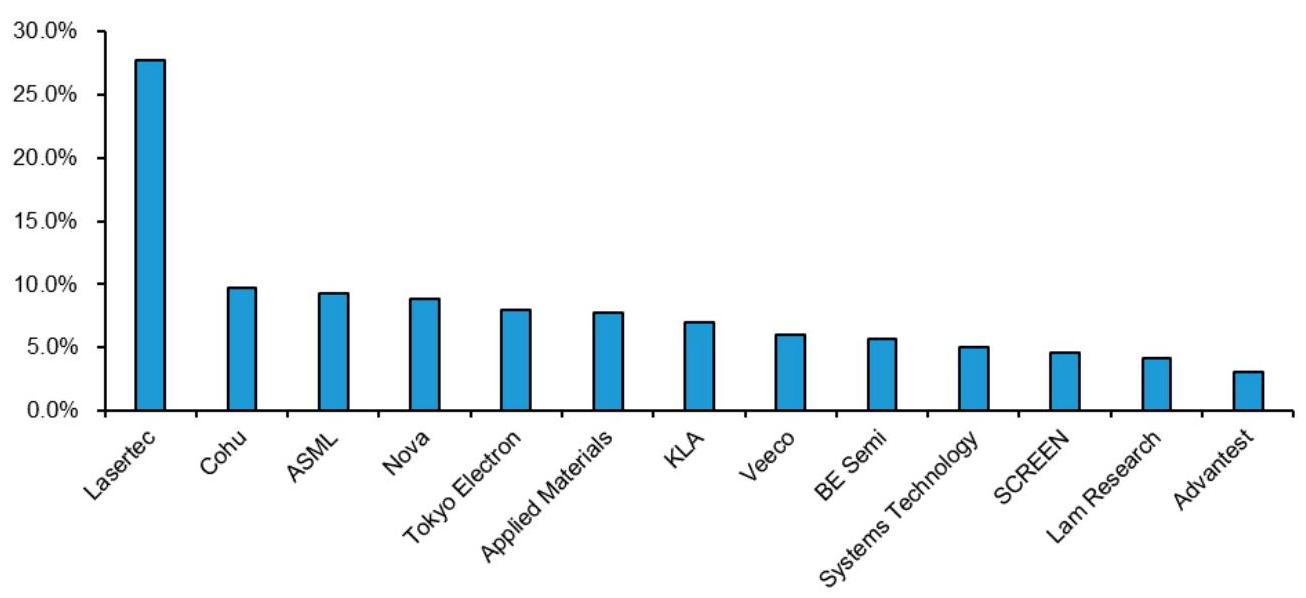

Key Suppliers' Exposure to Intel's Capex 主要供应商对Intel资本支出的敞口

Source: Bloomberg, Bernstein analysis. 来源:Bloomberg,Bernstein分析。

EUV Supply Chain Dependence EUV供应链依赖

-

Lasertec: derives up to 28% of its revenue from Intel, with Intel estimated to account for approximately 40% of its backlog.

-

ASML: receives 9.2% of its revenue from Intel, contributing 15-20% to its EUV revenue.

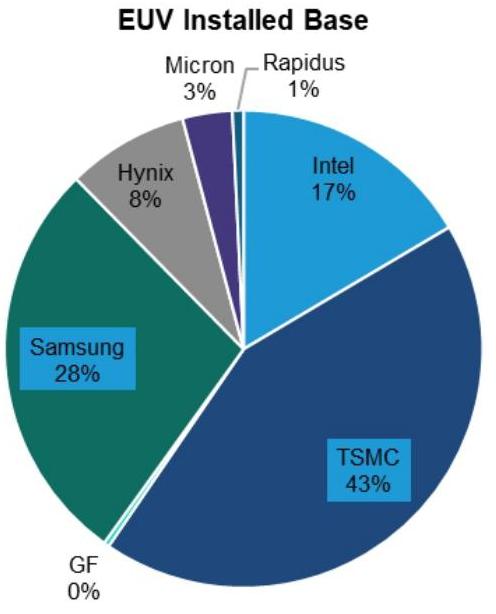

Intel's EUV Installed Base Intel的EUV已安装基数

Source: TechInsights, Bernstein analysis. 来源:TechInsights,Bernstein分析。

Intel's EUV installed base stands at 17%, making it one of the primary EUV users. Intel的EUV已安装基数达到17%,是主要的EUV用户之一。

High NA EUV Adoption Delay 高数值孔径EUV技术普及延迟

Intel was a potential early adopter of High NA|High Numerical Aperture EUV technology. If Intel ceases to advance new nodes, the widespread adoption of High NA could be delayed until TSMC's A10 node, approximately 2030. Intel是潜在High NA|高数值孔径 EUV技术的第一批采用者,若Intel不再推进新节点,High NA的普及可能推迟到TSMC的A10节点(约2030年)。

Overall Net Negative Impact on WFE Market 对WFE市场整体净负面影响

In the long term, Bernstein analysts believe that while Intel's capital expenditure will be replaced by other foundries (especially TSMC), this shift may still result in a net negative impact on the WFE market, estimated at a low single-digit percentage (LSD %), due to TSMC's higher efficiency in capital expenditure and utilization. 长期来看,Bernstein分析师认为,尽管Intel的资本支出将被其他晶圆代工厂(特别是TSMC)所取代,但由于TSMC在资本支出和利用率方面效率更高,这种转变对WFE市场总体而言仍可能造成一定程度的净负面影响,预计为低个位数百分比(LSD %)。

Impact on Semiconductor Material Suppliers 对半导体材料供应商的影响

Bernstein analysts foresee that Intel's strategic shift will benefit TSMC's suppliers, with Hoya being the most notable. Bernstein分析师认为,Intel的转变将利好TSMC的供应商,其中最值得关注的是Hoya。

EUV Photomask Substrate Market Share Shift EUV光掩模基板市场份额转移

Hoya is the exclusive supplier of TSMC's EUV photomask substrates, while AGC is the exclusive supplier for Intel. If Intel discontinues internal manufacturing, Hoya's share in the EUV photomask substrate market could theoretically increase from 70% to 100%, thereby taking over AGC's market share. Hoya是TSMC的EUV光掩模基板的独家供应商,而AGC是Intel的独家供应商。如果Intel停止内部制造,Hoya在EUV光掩模基板市场的份额理论上将从70%增长到100%,从而接管AGC的市场份额。

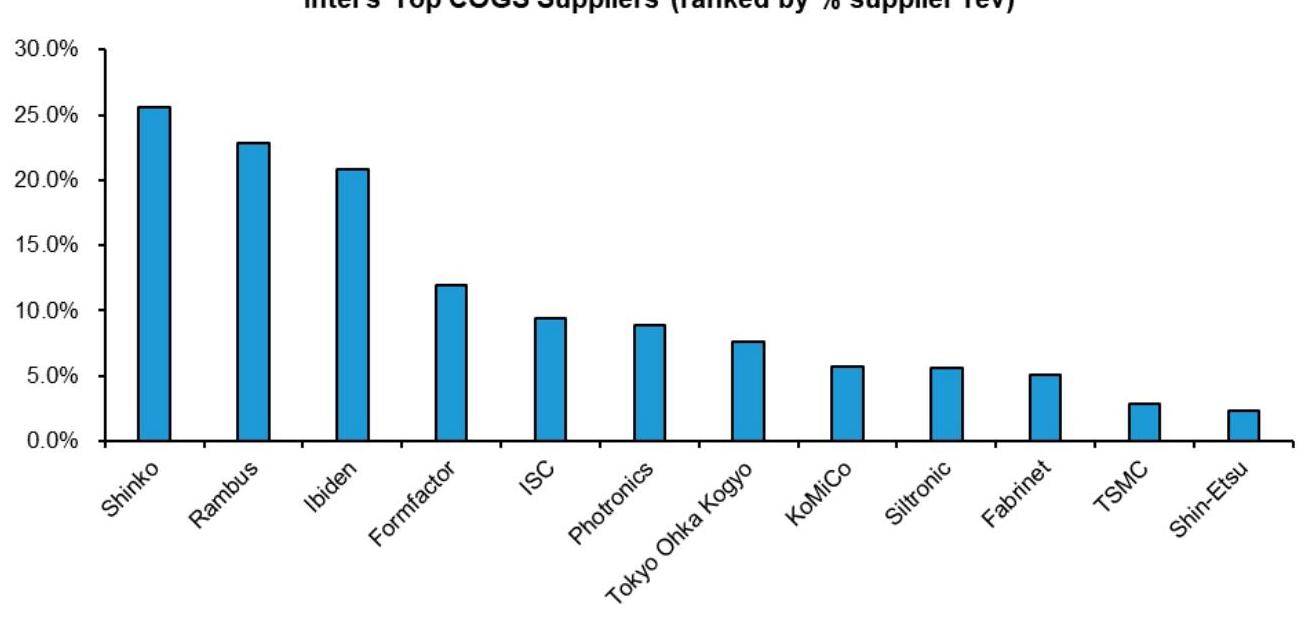

Intel's Main COGS Suppliers Intel的主要销售成本供应商

Source: Bloomberg, Bernstein analysis. 来源:Bloomberg,Bernstein分析。

Ibiden also has significant exposure to Intel, but is expected to remain unaffected, provided Intel continues to advance its backend packaging technology. Ibiden对Intel也有相当大的风险敞口,但预计将保持不受影响,前提是Intel继续推进其后端封装技术。

Impact on TSMC and Samsung Foundry 对TSMC和Samsung Foundry的影响

-

Bernstein analysts note a time lag between Intel's decision and the actual transition, given the need to redesign chips and establish capacity. Bernstein分析师指出,由于需要重新设计芯片和建立产能,从Intel做出决定到实际转变之间存在时间滞后。

-

If Intel shifts to a Fabless model, TSMC will be a clear beneficiary. 如果Intel转向Fabless模式,TSMC将明显受益。

-

Bernstein also believes that Intel's shared information confirms the strategic need for leading logic chip manufacturers to have alternative foundries beyond TSMC. Therefore, Samsung Foundry, being the best-positioned alternative, will also benefit. Bernstein认为,Intel分享的信息印证了其观点,即领先的逻辑芯片制造商在战略上需要TSMC之外的替代制造商,而Samsung Foundry是最佳定位的备选。因此,Samsung Foundry也将成为受益者。